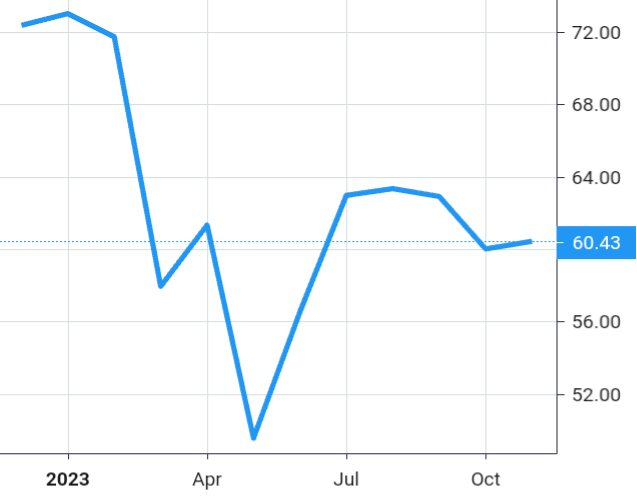

Stock Value

Stock Value

About MetLife

MetLife, Inc. (MetLife) operates as a financial services company worldwide.

The company provides insurance, annuities, employee benefits and asset management. The company holds leading market positions in the United States (‘U.S.’), Japan, Latin America, Asia, Europe and the Middle East. The company is also one of the largest institutional investors in the U.S. with a general account portfolio invested primarily in fixed income securities (corporate, structured products, municipals, and government and agency) and mortgage loans, as well as real estate, real estate joint ventures, other limited partnerships and equity securities.

In the fourth quarter of 2023, MetLife reorganized from five segments into the following six segments to reflect changes in management’s responsibilities: Group Benefits; Retirement and Income Solutions (‘RIS’); Asia; Latin America; Europe, the Middle East and Africa (‘EMEA’); and MetLife Holdings. The Group Benefits and RIS businesses were previously reported as the U.S. segment. In addition, the company continues to report certain of its results of operations in Corporate & Other.

The company distributes many of its products through a variety of third-party distribution channels, including banks and broker-dealers.

Segments and Corporate & Other

The company offers a broad range of products and services aimed at serving the financial needs of its customers. The company sells these products to corporations and other institutions (including local, state and federal governments) and their respective employees, as well as individuals.

Group Benefits

The company has built a leading position in the U.S. group insurance market through long-standing relationships with many of the largest employers in the U.S.

The company’s Group Benefits segment, based in the U.S., offers life insurance, dental, group short- and long-term disability, individual disability, accidental death and dismemberment (‘AD&D’) insurance, vision, and accident & health insurance, as well as prepaid legal plans and pet insurance. The company also sells administrative services-only (‘ASO’) arrangements to some employers.

The company distributes Group Benefits products and services through a sales force primarily consisted of MetLife employees that is segmented by the size of the target customer. Account executives sell either directly to corporate and other group customers or through an intermediary, such as a broker or consultant. Employers have been emphasizing voluntary products, and as a result, the company has increased its focus on communicating and marketing to employees in order to further foster sales of those products.

The company has entered into several operating joint ventures and other arrangements with third parties to expand opportunities to market and distribute Group Benefits products and services. The company also sells Group Benefits products and services through sponsoring associations and affinity groups and provide life, dental, accident & health, and vision coverage to certain employees of the U.S. Government. The company has longstanding relationships with these employees and continues to cultivate and expand them through additional product offerings.

Major Products

Term Life Insurance: A guaranteed benefit upon the death of the insured for a specified time period in return for the periodic payment of premiums. Premiums may be guaranteed at a level amount for the coverage period or may be non-level and non-guaranteed. Term contracts expire without value at the end of the coverage period when the insured party is still living.

Variable Life Insurance: Insurance coverage through a contract that gives the policyholder flexibility in investment choices and, depending on the product, in premium payments and coverage amounts, with certain guarantees. Premiums and account balances can be directed by the policyholder into a variety of separate account investment options or directed to the company’s general account. In the separate account investment options, the policyholder bears the entire risk of the investment results. With some products, by maintaining certain premium level, policyholders may have the advantage of various guarantees that may protect the death benefit from adverse investment experience.

Universal Life Insurance: Insurance coverage on the same basis as variable life, except that premiums, and the resulting accumulated balances, are allocated only to the company’s general account. With some products, by maintaining a certain premium level, policyholders may have the advantage of various guarantees that may protect the death benefit from adverse investment experience.

Dental: Insurance and ASO arrangements that assist employees, retirees and their families in maintaining oral health while reducing out-of-pocket expenses.

Disability: Insurance and ASO arrangements for groups and individuals to provide benefits for income replacement, payment of business overhead expenses or mortgage protection, in the event of the disability of the insured.

Accident & Health Insurance: Accident, critical illness or hospital indemnity coverage to the insured.

Vision: Insurance, ASO arrangements, and managed eye health and vision care solutions to assist employees, retirees and their families in maintaining vision health while reducing out-of-pocket expenses. Offered to commercial groups, individuals, health plans and government sponsored programs through a nationwide provider network, retail optical chains and online eyewear providers.

Retirement and Income Solutions

The company’s RIS segment, based in the U.S., provides funding and financing solutions that help institutional customers mitigate and manage liabilities primarily associated with their employee benefit programs using a spectrum of life and annuity-based insurance and investment products.

The company distributes RIS products and services through dedicated sales teams and relationship managers primarily consisted of MetLife employees. The company may sell products directly to benefit plan sponsors and advisors or through brokers, consultants or other intermediaries. In addition, these sales professionals work with individual, group and global distribution areas to better reach and service customers, brokers, consultants and other intermediaries.

Major Products

Stable Value Products

General account guaranteed interest contracts (‘GICs’) are designed to provide stable value investment options within tax-qualified defined contribution plans by offering a fixed maturity investment with a guarantee of liquidity at contract value for participant transactions.

Separate account GICs are available to defined contribution plan sponsors by offering market value returns on separate account investments with a general account guarantee that plan participants will always be able to transact in their accounts at contract value.

Synthetic GICs or ‘wraps’ are contracts available only to the sponsor of a participant-directed defined contribution plan. The contract ‘wraps’ a portfolio of investments owned by the plan to provide a guarantee that plan participants will always be able to transact in their accounts at contract value. Generally, a wrap contract means that participants will not experience negative returns.

Private floating rate funding agreements are generally privately-placed, unregistered investment contracts issued as general account obligations with interest credited based on a specified rate or agreed upon short-term benchmark rate. These agreements are used for money market funds, securities lending cash collateral portfolios and short-term investment funds.

Annuities

Pension Risk Transfers

General account and separate account annuities are offered in connection with defined benefit pension plans, which include single premium buyouts allowing for full or partial transfers of pension liabilities.

General account annuities include non-participating group contract benefits purchased for retired or active employees covered under terminating or ongoing pension plans.

Separate account annuities include both participating and non-participating group contract benefits. Participating contract benefits are purchased for retired, terminated, or active employees covered under active or terminated pension plans. The assets supporting the guaranteed benefits for each contract are held in a separate account, however, the company fully guarantees all benefit payments. Non-participating contracts have economic features similar to the company’s general account product, but offer the added protection of an insulated separate account.

Institutional Income Annuities: General account contracts that are guaranteed payout annuities purchased for employees upon retirement or termination of employment. Contracts can be life or non-life contingent non-participating contracts which do not provide for any loan or cash surrender value and, with few exceptions, do not permit future considerations.

Structured Settlements: Customized annuities designed to serve as an alternative to a lump sum payment in a lawsuit initiated because of personal injury, wrongful death, or a workers’ compensation claim or other claim for damages. Surrenders are generally not allowed, although commutations are permitted in certain circumstances. Guaranteed payments consist of life contingent annuities, term certain annuities and lump sums.

Risk Solutions:

Longevity Reinsurance Solutions

Longevity reinsurance is a risk mitigation solution for the United Kingdom (‘U.K.’) pension plan sponsors and the U.K. insurance companies that write pension risk transfer business, converting uncertain future pension benefit obligations into a fixed stream of payments to MetLife over the duration of the contract as opposed to a lump sum at inception in typical pension risk transfer transactions.

Benefit Funding Solutions: Specialized life insurance products and funding agreements designed specifically to provide solutions for funding postretirement benefits and company-, bank- or trust-owned life insurance used to finance nonqualified benefit programs for executives.

Capital Markets Investment Products

Funding agreement-backed notes are offered in medium term note programs, under which funding agreements are issued to special-purpose trusts that issue marketable notes in the U.S. dollars or foreign currencies. The proceeds of these note issuances are used to acquire funding agreements with matching interest and maturity payment terms from certain subsidiaries of MetLife. The notes are underwritten and marketed by major investment banks’ broker-dealer operations and are sold to institutional investors.

Funding agreement-backed commercial paper is issued by a special-purpose limited liability company, which deposits the proceeds under a master funding agreement issued to it by Metropolitan Life Insurance Company (‘MLIC’). The commercial paper is issued in the U.S. dollars or foreign currencies, receives the same short-term credit rating as MLIC and is marketed by major investment banks’ broker-dealer operations.

Funding agreements are issued by certain of the company’s insurance subsidiaries to the Federal Home Loan Bank of New York (‘FHLBNY’) and to a subsidiary of the Federal Agricultural Mortgage Corporation.

Asia

The company’s Asia operations are geographically diverse encompassing both developed and emerging markets. The company operates in nine jurisdictions throughout Asia, with its largest operation in Japan. The company markets its products and services through a range of proprietary and third-party distribution channels.

In Japan, the company’s face-to-face channels, including both career and general agency, continue to be critical to the company’s overall distribution strategy, catering to various needs of individual retail customers. In select markets, the company also uses independent brokers for retail sales and the company’s employee sales force to sell group products.

Major Products

Life Insurance: Whole and term life, endowments, universal and variable life, as well as group life products.

Accident & Health Insurance: Full range of accident & health products, including hospitalization, cancer, critical illness, disability, income protection and personal accident coverage.

Retirement and Savings: Fixed and variable annuities, as well as regular savings products.

Latin America

The company’s largest operations are in Mexico and Chile. The company markets its products and services through a multi-channel distribution strategy, which varies by geographic region and stage of market development.

The company has an exclusive and captive agency distribution network, which sells a variety of individual life, accident & health, and pension products. The company’s direct marketing channel includes sponsors and telesales representatives selling mainly accident & health and individual life products directly to consumers. The company also works with brokers and independent agents on sales of group and individual life, accident and health, group medical, dental and pension products, and worksite marketing. The company also offers to government employees life and medical insurance, as well as retirement and savings, and other products.

Major Products

Life Insurance: Whole and term life, endowments, universal and variable life, as well as group life products.

Retirement and Savings: Fixed annuities and pension products. Fixed income annuities provide for asset distribution needs. The company’s savings-oriented pension products are primarily offered in Chile under a mandatory privatized social security system.

Accident & Health Insurance: Group and individual major medical, accidental, and supplemental health products, including AD&D, hospital indemnity, medical reimbursement, and medical coverage for serious medical conditions, as well as dental products.

Credit Insurance: Policies designed to fulfill certain loan obligations in the event of the policyholder’s death.

EMEA

The company operates across EMEA in both developed (Western Europe) and emerging (Central and Eastern Europe, the Middle East and Africa) markets. The company’s largest operations are in the Gulf region, the U.K. and France. In more mature markets, the company focuses its strategy on its preferred market segments to play a ‘niche’ role. The company also has a strong market presence in emerging markets leveraging a multi-channel distribution strategy.

The company’s businesses in EMEA use captive and independent agency, independent brokerage, bancassurance, corporate solutions and direct-to-consumer distribution channels.

Major Products

Life Insurance: Traditional and non-traditional life insurance products, such as whole and term life, endowments and variable life products, as well as group term life programs in most markets.

Retirement and Savings: Fixed annuities and pension products, including group pension programs in select markets.

Accident & Health Insurance: Individual and group personal accident and supplemental health products, including AD&D, hospital indemnity, scheduled medical reimbursement plans, and coverage for serious medical conditions. In addition, the company provides individual and group major medical coverage in select markets.

Credit Insurance: Policies designed to fulfill certain loan obligations in the event of the policyholder’s death.

MetLife Holdings

This segment consists of operations relating to products and businesses that the company no longer actively market in the U.S. These include variable, universal, term and whole life insurance, variable, fixed and index-linked annuities, and long-term care insurance. It also includes an in-force block of assumed variable annuity guarantees from a third party.

Major Products

Variable, Universal and Term Life Insurance: Similar to products offered by the company’s Group Benefits segment, except that these products were historically marketed to individuals through various retail distribution channels.

Whole Life Insurance: A benefit upon the death of the insured in return for the periodic payment of a fixed premium over a predetermined period. Whole life insurance includes policies that provide a participation feature in the form of dividends. Policyholders may receive dividends in cash, or apply them to increase death benefits, increase cash values available upon surrender or reduce the premiums required to maintain the contract in-force.

Variable Annuities: Variable annuities provide for asset accumulation and asset distribution needs. Variable annuities allow the contractholder to allocate deposits into various investment options in a separate account, as determined by the contractholder. In certain variable annuity products, contractholders may also choose to allocate all or a portion of their account to the company’s general account and are credited with interest at rates the company determines, subject to specified minimums. Contractholders may also elect certain minimum death benefit and minimum living benefit guarantees for which additional fees are charged and where asset allocation restrictions may apply.

Fixed and Indexed-Linked Annuities: Fixed annuities provide for asset accumulation and asset distribution needs. Deposits made into deferred annuity contracts are allocated to the company’s general account and are credited with interest at rates the company determines, subject to specified minimums. Fixed income annuities provide a guaranteed monthly income for a specified period of years and/or for the life of the annuitant. Additionally, the company has issued indexed-linked annuities which allow the contractholder to participate in returns from equity indices.

Long-term Care: Protection against the potentially high costs of long-term health care services. Generally pays benefits to insureds who need assistance with activities of daily living or have a cognitive impairment.

Corporate & Other

Corporate & Other contains various start-up, developing and run-off businesses.

Regulation

In the U.S., state regulators primarily regulate the company’s life insurance companies, with additional federal regulation of some of the company’s products and services. The insurance holding company laws of various U.S. jurisdictions apply to MetLife, Inc. and its U.S. insurance subsidiaries. Furthermore, consumer protection laws, privacy, anti-money laundering, securities, commodities, broker-dealer and investment adviser regulations, environmental and unclaimed property laws and regulations, and the Employee Retirement Income Security Act of 1974 (‘ERISA’) also apply to some of MetLife’s operations, products and services.

The Dodd-Frank Wall Street Reform and Consumer Protection Act (‘Dodd-Frank’) increased the potential federal role in regulating businesses, such as the company.

The company is subject to the U.S. state insurance holding company laws and regulations that are generally based on the National Association of Insurance Commissioners’ (‘NAIC’) Insurance Holding Company System Regulatory Act and Regulation (‘Model Holding Company Act and Regulation’).

MetLife’s lead state regulator is the New York State Department of Financial Services (NYDFS).

The European Insurance and Occupational Pensions Authority along with European legislation, requires European regulators, such as the Central Bank of Ireland, to establish supervisory forums for European Economic Area (‘EEA’)-based insurance groups with significant European operations, including MetLife.

The company’s insurance business throughout the EEA is subject to the Solvency II Directive and its implementing rules. In China, the business of the company’s joint venture (as well as the industry) has implemented China Risk Oriented Solvency System (‘C-ROSS’), a risk-based solvency regime.

The NYDFS promulgated the New York Cybersecurity Requirements for Financial Services Companies (the ‘Regulation’) to promote the protection of customer information and information technology systems by establishing and regulating cybersecurity requirements for banking and insurance entities under the NYDFS’s jurisdiction. In general, the Regulation requires covered entities, such as the company’s insurance entities licensed in New York, to assess risks associated with their information systems and establish and maintain a cybersecurity program designed to assess those risks and protect the confidentiality, integrity and availability of such systems and data.

In the U.S., the company is subject to state laws, which impose certain obligations on the processing of personal information and provide consumers specific rights to control their personal information. For instance, the California Consumer Privacy Act (‘CCPA’), which applies to certain portions of the company’s business, requires covered companies to provide disclosures to California consumers about such companies’ data collection, use and sharing practices and gives California residents expanded rights with respect to the processing of their personal information. In 2020, the CCPA was amended by the California Privacy Rights Act, which took effect in most material respects in 2023 and imposes additional rights and obligations. While a significant portion of the company’s business is exempted from the CCPA’s specific requirements, the Health Insurance Portability and Accountability Act and the insurance laws of several states to which the company is subject grant similar rights to insureds, including the right to request copies of their personal information that a company has collected.

Outside of the U.S., the company’s subsidiaries are subject to various data protection regimes, including the General Data Protection Regulation (EU) 2016/679 (‘GDPR’), which became effective in May 2018, and applies to entities established in the EU, as well as to entities not established in the EU, that target goods or services to EU data subjects, or that monitor consumer behavior that takes place in the EU.

The company is also subject to increasingly restrictive laws in other jurisdictions that address and impose strict requirements on cross-border data transfers, including for example, China’s Personal Information Protection Law. The company continues to monitor the developments of the Artificial Intelligence Act and other governmental initiatives around the world, particularly in jurisdictions where the company operates.

The company provides products and services to certain employee benefit plans that are subject to ERISA and/or Section 4975 of the Internal Revenue Code of 1986, as amended (the ‘Code’).

In New York, the NYDFS expects both New York domestic insurers, such as MLIC, and foreign authorized insurers, such as the company’s other insurance subsidiaries licensed in New York, to manage material climate risks by taking actions that are proportionate to the nature, scale and complexity of their businesses.

Although the consumer financial services subject to the CFPB’s jurisdiction generally exclude insurance business of the kind in which the company engages, the CFPB does have authority to regulate non-insurance consumer services the company provides.

Some of the company’s subsidiaries and their activities in offering and selling variable insurance products are subject to extensive regulation under the federal securities laws and regulations administered by the SEC. These subsidiaries issue variable annuity contracts and variable life insurance policies with separate accounts that are registered with the SEC as investment companies under the Investment Company Act of 1940, as amended (the ‘Investment Company Act’) or are exempt from registration under the Investment Company Act. Such separate accounts are generally divided into sub-accounts, each of which invests in an underlying mutual fund which is itself a registered investment company under the Investment Company Act. In addition, the variable annuity contracts and variable life insurance policies associated with these registered separate accounts are registered with the SEC under the Securities Act of 1933, as amended (the ‘Securities Act’) or are exempt from registration under the Securities Act.

Two of the company’s U.S. subsidiaries are registered with the SEC as broker-dealers under the Securities Exchange Act of 1934, as amended (‘Exchange Act’) and are members of, and subject to regulation by, FINRA. The SEC, CFTC and FINRA from time to time propose and adopt rules and regulations that impact broker-dealers and products deemed to be securities.

Two of the company’s U.S. subsidiaries are registered as investment advisers with the SEC under the Investment Advisers Act of 1940, as amended, and one is also registered or licensed in various non-U.S. jurisdictions, as applicable. In addition, the company has non-U.S. subsidiaries that are registered or licensed in non-U.S. jurisdictions to conduct the company’s investment management business.

One of the company’s U.S. broker-dealers serves as the principal underwriter and distributor of these variable products and other securities offerings. The company’s broker-dealer distributes these products via unaffiliated third party broker-dealers and financial intermediaries that sell these products to end investors. Under SEC rules, the selling broker-dealers recommending the company’s variable products and other securities offerings to end investors are required to comply with various SEC and FINRA rules and regulations, including Regulation Best Interest. SEC rules also require these selling broker-dealers to disclose the nature of services, their standard of conduct, and their conflicts of interest to their retail customers. With regard to insurance products, the NAIC revised its Suitability in Annuity Transactions Model Regulation to add a ‘best interest’ standard for the sale of annuities, which most of the company’s insurance subsidiaries’ domiciliary states adopted and others may consider.

Federal and state securities regulatory authorities and FINRA from time to time make inquiries and conduct examinations regarding compliance by MetLife and its subsidiaries with securities and other laws and regulations.

Trademarks

The company has a worldwide trademark portfolio that it considers important in the marketing of its products and services, including among others, the trademark ‘MetLife.’ The company also has trademarks, such as the ‘PROVIDA’ trademark, the company has acquired with businesses.

History

MetLife, Inc. was founded in 1863. The company, a Delaware corporation, was incorporated in 1999.